“Post-Fed whiplash.” The week opened with a positioning purge: leveraged longs were forced out, spot ETFs bled mid-week, and price briefly knifed lower before macro steadied the tape. The Fed’s preferred inflation gauge (PCE) printed in line, keeping the easing path intact and arresting the drawdown into Friday’s close. Under the surface, issuers prepared for new ETF launches after last week’s SEC rule change, Tether shuffled senior leadership as it readies USAT, and listed miners doubled down on AI/HPC pivots to smooth cash flows. Policy divergence remained in focus (SNB steady; BoE debate; Tokyo inflation firm), but none of it undercut the core thesis: policy support is alive; the early-week selloff was about positioning, not fundamentals.

Price Action & Flows

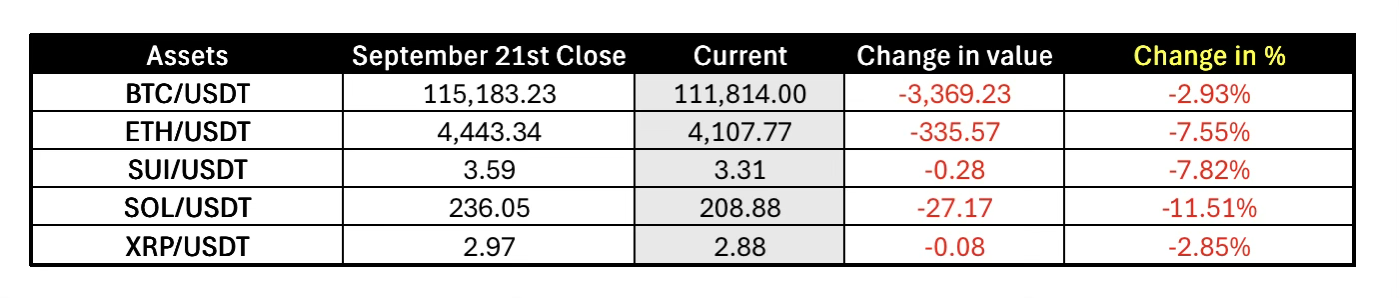

The first 48 hours were rough: a broad risk shakeout wiped out crowded longs, took BTC briefly below recent supports, and pushed majors into forced-seller territory. The signal came through ETF tape by mid-week: U.S. spot BTC ETFs posted a ~$258M net outflow on Sep 25, a sharp reversal from the heavy net buying earlier in the month. By Friday, on-consensus PCE prints calmed nerves and stemmed the bleeding. Net-net, the week reads as positioning washout → macro reassurance → tentative rebuild.

- Liquidations: ~$1.5-1.8B cleared in a two-day window as perp leverage reset.

- ETF pulse: ~$258M BTC out on Sep 25 (most issuers negative), underscoring fragile post-cut positioning.

- Rotation: SOL momentum cooled with price slipping from recent highs; OI stayed elevated - a setup for two-way volatility if fresh ETF headlines land.

Macro & Policy - Data Recap (Sep 22-28)

The macro arc this week was “no new drama, cuts still in play.” Fed commentary framed the path after the September trim, and then PCE - the Fed’s favorite thermometer - arrived exactly as penciled: headline +0.3% m/m; core +0.2% m/m; core y/y 2.9%. Markets exhaled: nothing here to derail the easing trajectory or revive “sticky inflation” chatter. That’s why the de-risking faded into Friday - the data reaffirmed the soft-landing glidepath rather than challenge it.

Other data painted a nuanced picture:

- German PMIs (Sep 23): Manufacturing slumped to 48.5 (exp 50.0) while Services surprised at 52.5 (exp 49.5).

- U.S. PMIs (Sep 23): Manufacturing 52.0 (slightly under exp 52.2), Services 53.9 (just under exp 54.0).

- Powell speech (Sep 23): Emphasized a data-dependent stance, reiterated patience after September’s cut.

- U.S. Final GDP (Sep 24): 3.8% q/q vs. 3.3% expected, showing resilience.

- U.S. Jobless Claims (Sep 25): 218K vs. 233K expected - softer labor market.

- Core PCE (Sep 26): +0.2% m/m (in line, steady vs. prior).

Meanwhile, divergence abroad kept investors cautious. The SNB held at 0.00% on Sep 25 and signaled a steady hand amid tariffs and soft external demand. In the UK, MPC’s Swati Dhingra warned against being “overly cautious,” pushing for faster cuts. In Japan, Tokyo core CPI held above 2%, keeping late-October BoJ hike risk alive.

Takeaway: The selloff was a positioning event, not a macro shock. On-consensus PCE and softer claims kept the easing runway clear - the bull case bent, not broken.

Regulation & Legal

The most market-relevant development came from Washington, but technically the week before. On Sep 17, the SEC approved “generic listing standards” for commodity-based trust shares, which means qualifying spot crypto ETFs can now list without a separate approval process each time. This week, issuers and exchanges began lining up new products and preparing filings under the streamlined rules. The change should deepen liquidity and broaden the ETF product shelf into Q4-Q1 once risk appetite stabilizes.

In Europe and the UK, the regulatory tape was quieter, with MiCA implementation cadence and the BoE’s policy debate providing the backdrop. But the clear regulatory driver for markets right now is the U.S. ETF pipeline.

Corporate, ETFs & On-Chain

Tether deepens its bench ahead of USAT. Tether appointed Benjamin Habbel (ex-Google, ex-Limestone) as Chief Business Officer on Sep 24, with a broad remit across growth, finance, investments, and portfolio expansion spanning AI, mining, energy, cloud, and infra. Strategically, it signals Tether’s intent to operate as “The Stable Company,” while building a U.S.-compliant lane via USAT - a dual-track approach (global USDT + U.S.-regulated USAT) that could reshape stablecoin competition versus USDC.

Miners tilt toward AI/HPC cash flows. IREN said it doubled AI cloud capacity by adding ~12,400 GPUs (to ~23,000 total), projecting >$500M run-rate revenue by early 2026. Bitdeer also drew attention as street targets moved higher on HPC prospects while self-mining hashrate ramped toward 40 EH/s by October. The mosaic: listed miners are building revenue streams less correlated with hash-price cycles, a positive for equity multiples and balance-sheet resilience into 2026.

ETF pulse check. After one of the biggest mid-September net-inflow weeks, Sep 25 saw spot Bitcoin ETFs flip to net outflows (~$258M), with most issuers negative on the day. The question for the coming week is whether that was a one-off de-risking after the Fed, or the start of a lighter tape until the next macro catalyst.

Solana DAT Spotlight - Nasdaq Listing and Expansion

A major storyline around Solana treasury vehicles continued this week. SOL Strategies - which began trading on Nasdaq on Sep 9 (STKE) - drew renewed attention as the DAT++ model matured. The company now holds more than 435,000 SOL, operates validator networks acquired from Orangefin, Cogent, and Laine, and reported nearly $800,000 in positive adjusted EBITDA for Q3. Institutional-grade governance (SOC and ISO certifications) was highlighted as part of the pitch to mainstream investors.

Momentum in the DAT space wasn’t confined to a single firm. DeFi Development Corp (DFDV), another Nasdaq-listed vehicle, announced South Korea’s first Solana treasury through a partnership with Fragmetric Labs and simultaneously boosted its buyback program to $100 million on Sep 24.

The broader DAT flywheel remains in focus: when DAT stocks trade at a premium to NAV, companies can issue new shares to acquire more crypto and compound their per-share exposure; when sentiment reverses, the mechanism can flip into dilution or forced sales. This week underscored that Solana’s DAT ecosystem is no longer niche - multiple publicly listed firms are now positioning themselves as gateways for traditional capital into SOL.

What We’re Watching Next (Sep 29-Oct 6)

Macro & Data:

- Sep 30: U.S. JOLTS Job Openings (prior 7.18M; expected 7.15M).

- Oct 1: ADP Non-Farm Employment Change (exp 53K; prior 54K). ISM Manufacturing PMI (exp 49.1; prior 48.7).

- Oct 2: U.S. Unemployment Claims (exp 229K; prior 218K).

- Oct 3: BoJ Gov Ueda speaks. U.S. jobs report - NFP (exp 51K; prior 22K), Unemployment Rate (exp 4.3%), Avg. Hourly Earnings (exp 0.3%). ISM Services PMI (exp 52.0; prior 52.0).

ETFs: Do BTC/ETH ETF flows snap back post-PCE? Watch for first movers using the SEC’s new generic standards - any filings under the pathway will be a read-through on breadth and timing into Q4.

Stablecoins: USAT build-out milestones (banking rails, disclosures) and whether Tether’s org expansion accelerates that timetable.

Miners & AI: Additional GPU capacity announcements and cloud-revenue updates from listed miners (IREN, BTDR) as the market prices non-hash cash flows.

Policy divergence: SNB’s hold aftermath on CHF; BoE rhetoric (Dhingra/Greene contrast) for cut timing; BoJ guidance into late-Oct with Tokyo CPI above 2%.

Disclaimer:

The information provided in this newsletter is for informational purposes only and should not be considered financial, investment, or legal advice. Please consult with a qualified professional before making any investment or financial decisions. Past performance is not indicative of future results, and all investments carry risks, including the potential loss of principal.

Disclaimer:

The information provided in this article is for informational purposes only and should not be considered financial, investment, or legal advice. Please consult with a qualified professional before making any investment or financial decisions. Past performance is not indicative of future results, and all investments carry risks, including the potential loss of principal.